Weekly Report 4

Unified margin drastically reduces your liquidation risk compared to isolated-margin venues and increases your borrowing capacity.

What you probably missed from last week on P0

JLP type strategies became the dominant player on the platform.

Stablecoin strategies became more attractive.

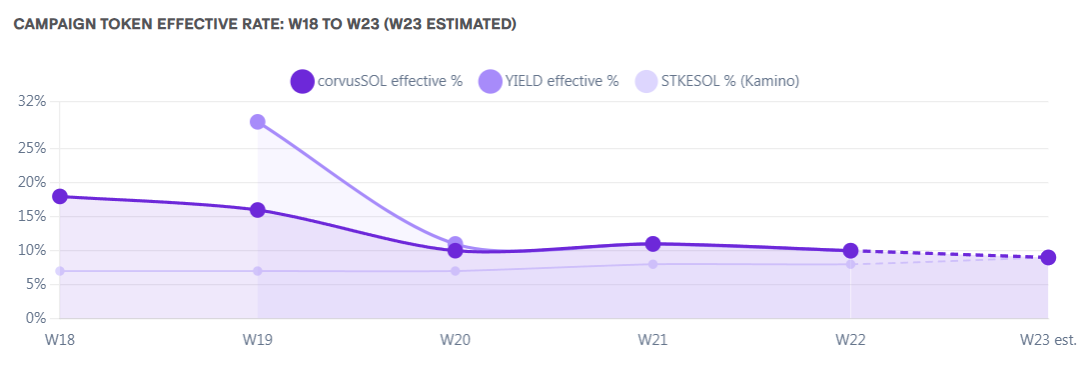

Campaign assets diverged: corvusSOL and YIELD lost momentum, while STKESOL continued to strengthen and expand.

The result is a platform increasingly driven by sustainable yield sources, stablecoin strategies, and directional opportunities rather than short-term incentives.

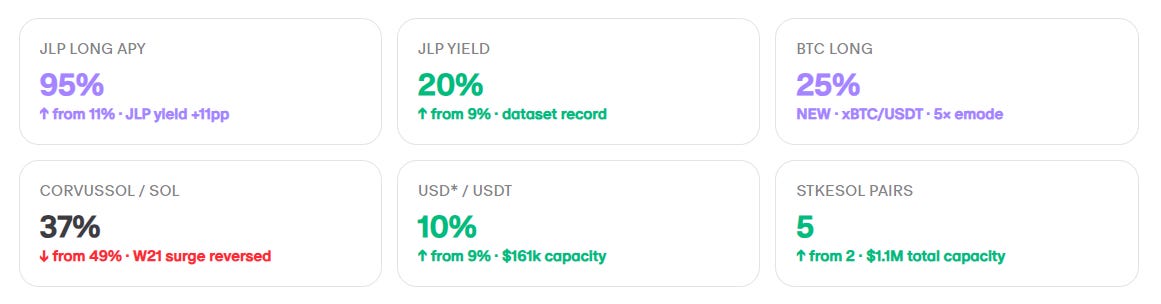

Best Opportunities Right Now

High Yield

JLP Long (95%)

BTC Long (25%)

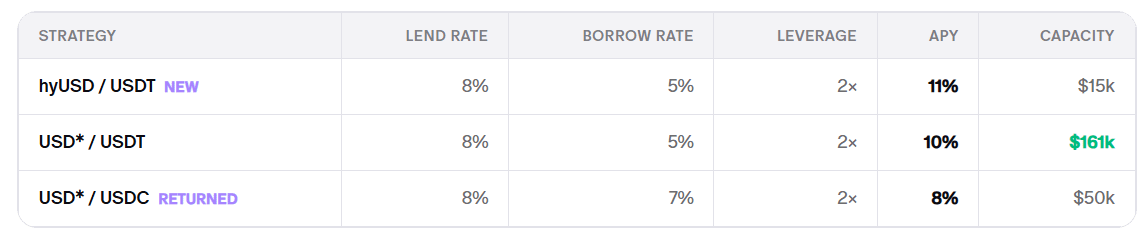

Stablecoin Strategies

hyUSD / USDT (11%)

USD / USDT* (10%)

USD / USDC* (8%)

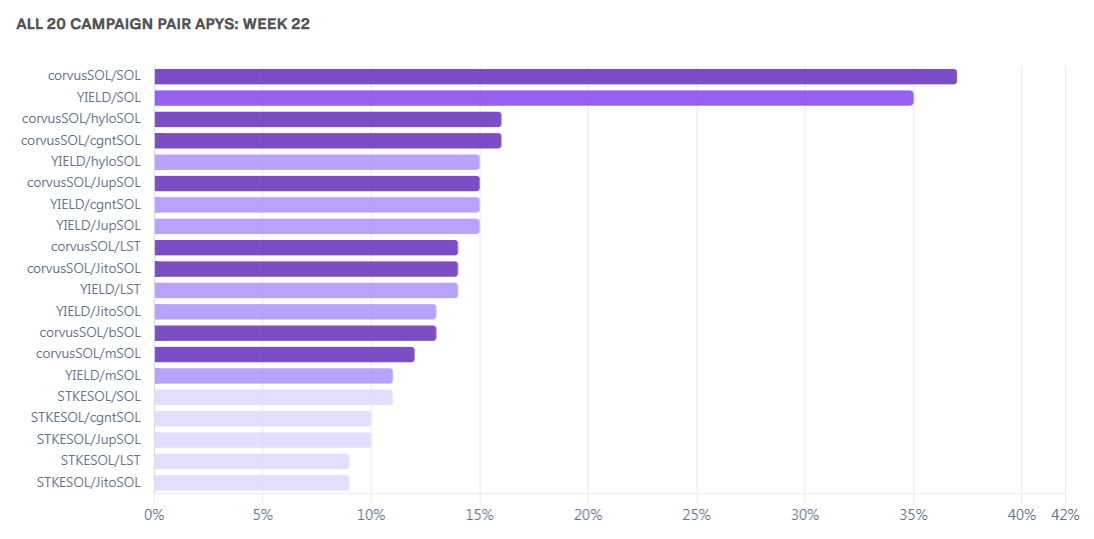

Campaign Strategies

corvusSOL / SOL (37%)

STKESOL ecosystem strategies (8–11%)

Snapshot

This is a quick metric overview on P0 strategies update.

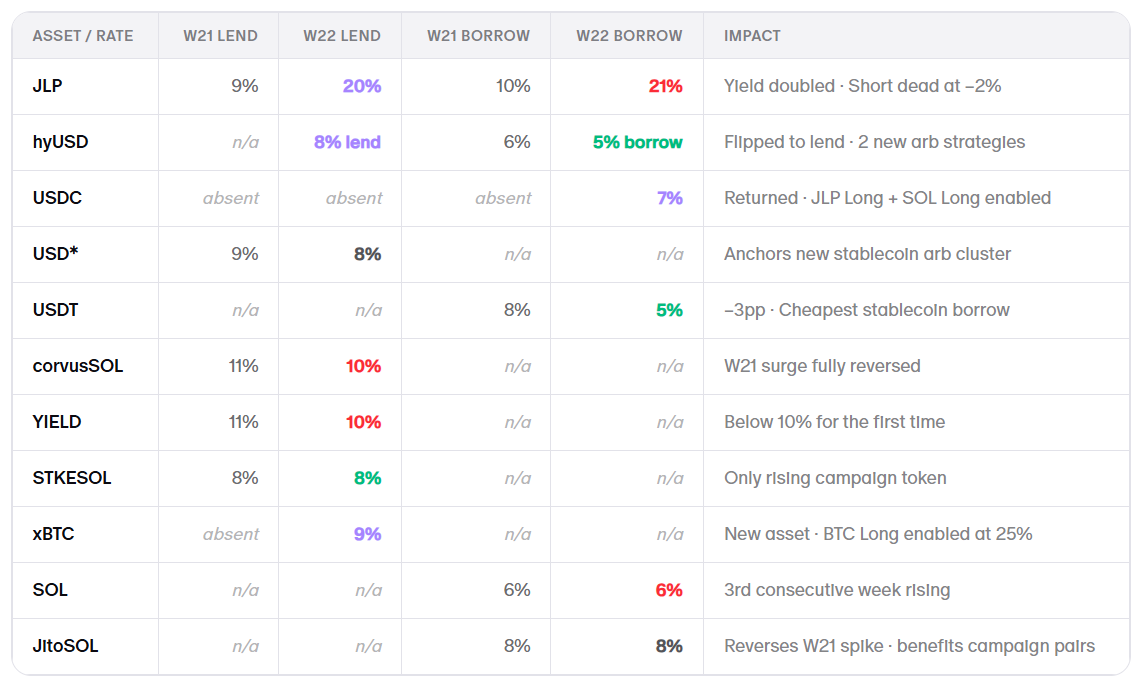

Rate Snapshot

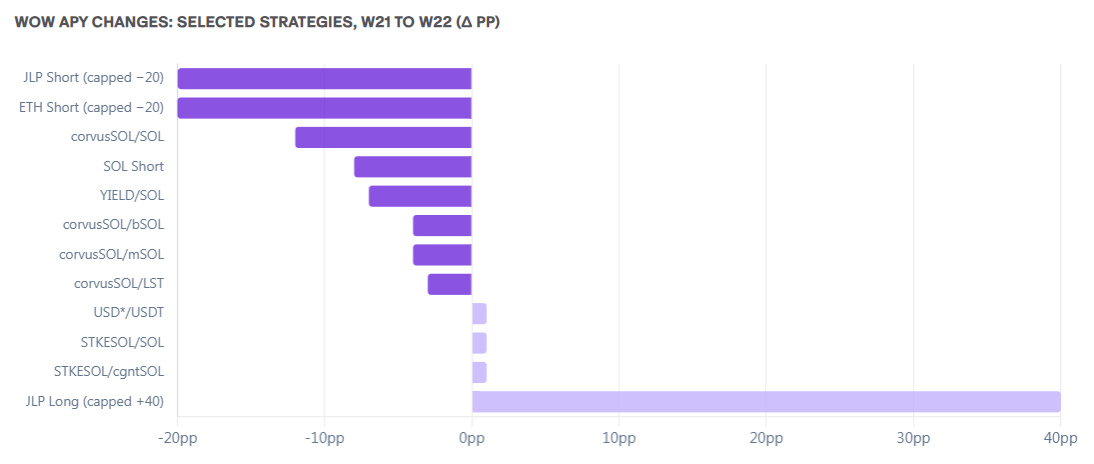

The Table and bar chart below compare the variation in rates between week 21 & week 22

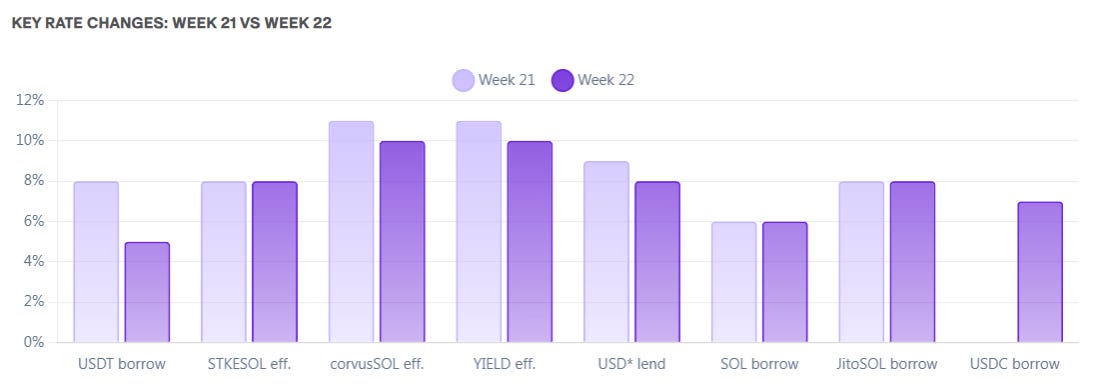

This chart compares the key lending, borrowing, and campaign-token rates between Weeks 21 and 22

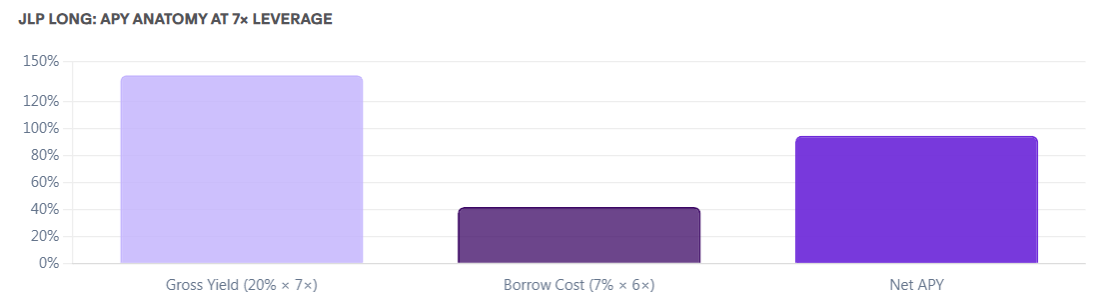

JLP is gaining momentum

JLP yield more than doubled from 9% to 20%, driven by stronger revenue generation from Jupiter Perpetuals. Combined with the return of USDC borrowing, this transformed JLP Long from a mid-tier strategy into the highest APY opportunity on the platform at 95%.

Unlike many campaign-based yields, JLP returns are generated from actual trading activity, including fees, spreads, and liquidations. This makes it one of the few strategies whose yield is tied directly to platform usage rather than token incentives.

Stablecoins Are Back

USDT borrowing costs fell from 8% to 5%, while hyUSD introduced a new lending opportunity at 8%. Together with USD*, this created a new group of stablecoin strategies generating between 8% and 11% APY.

These strategies offer a different profile from directional trades or campaign farming. They have no direct exposure to crypto price movements and provide some of the largest deployable capacities currently available on the platform.

For users looking for more conservative returns, stablecoins became one of the strongest categories in Week 22.

This table compares three stablecoin arbitrage strategies.

This chart visualizes the trade-off between APY and available capacity across the three strategies.

Campaign Strategies Begin to Normalize

Campaign yields lost momentum this week.

corvusSOL gave back most of its Week 21 gains, falling from 11% to 10%, while YIELD dropped below 10% for the first time and lost several strategy pairs.

STKESOL was the exception.

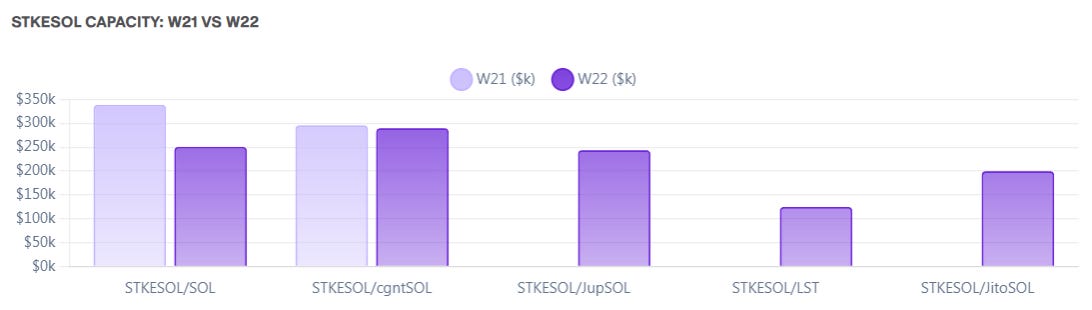

The asset posted a second consecutive week of growth, added three new pairs, and nearly doubled available capacity. It is now the only campaign token showing a consistent upward trend and is beginning to close the gap with YIELD.

While campaign opportunities remain attractive, the category is becoming increasingly competitive and less dominant than it was just a few weeks ago.

This chart tracks weekly effective APYs for corvusSOL, YIELD, and STKESOL, showing campaign yields converging toward ~9–10% by W23 after earlier spikes, with STKESOL the only strategy trending slightly upward.

This chart ranks all campaign-token pair strategies by APY, showing corvusSOL/SOL and YIELD/SOL as the highest-yielding opportunities at roughly 37% and 35%, respectively.

This chart compares deployable capacity across STKESOL pairs between Weeks 21 and 22, showing total capacity growth of about 75% to $1.1M driven by the addition of three new pairs

Directional strategies are still a good play

Week 22 introduced two new directional strategies.

BTC Long launched through xBTC/USDT at 25% APY, while SOL Long appeared for the first time using corvusSOL and USDC at 14% APY.

These strategies allow users to gain leveraged exposure to market upside while still earning yield, expanding the platform beyond traditional farming and arbitrage opportunities.

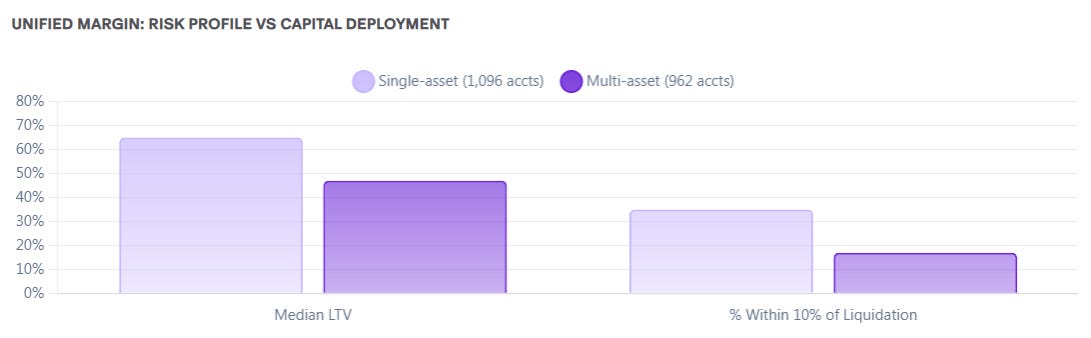

Reduce you risk exposition and improve your capital efficiency with the unified margin

P0 runs a cross-margin model. One collateral deposit supports multiple borrow positions simultaneously. This is game changer from a capital efficiency perspective.

On an isolated-margin platform, each strategy requires its own capital allocation. On P0, the same deposit backs all active positions at once. The protocol nets total collateral against total borrow exposure, applying risk weights per asset class. Run a campaign pair, a stablecoin arb, and a directional long from a single margin pool. Portfolio yield is the weighted average of every active position.

With 33 strategies live this week, ranging from 8% STKESOL pairs to 95% JLP Long, unified margin changes the capital efficiency equation significantly. Capital serving as collateral on a low-volatility position contributes to the liquidation buffer on a higher-leverage one.

eMode compounds this further. Correlated asset pairs (corvusSOL/SOL, STKESOL/JitoSOL) carry lower risk weights by design, allowing higher leverage on the same collateral base. The protocol prices correlation risk correctly and passes that efficiency to the user.

Platform data confirms this across all active accounts:

Multi-asset accounts hold 51% more collateral and 22% more borrow value on average. Their share at imminent liquidation risk is 2× lower (17% vs 35%).

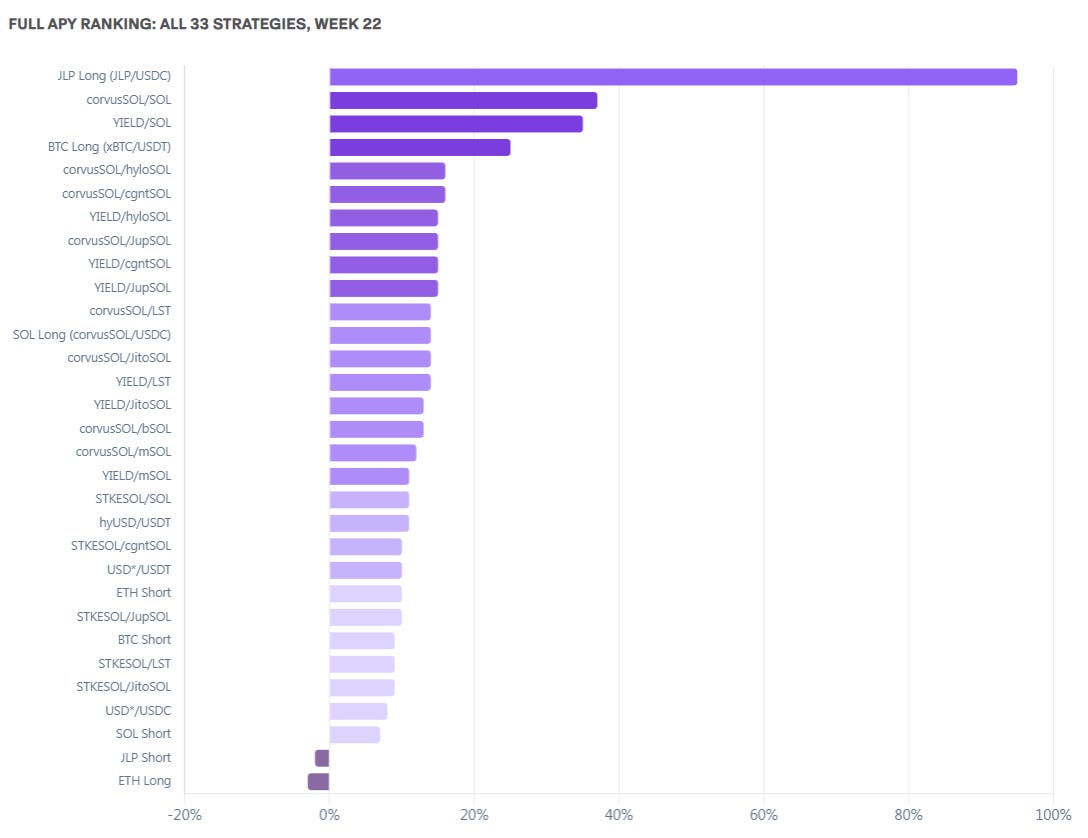

Full APY Ranking

This chart ranks every strategy by APY, highlighting that directional trades dominate the top of the leaderboard while campaign, stablecoin, and a few negative-yield strategies occupy the middle and lower ranges.

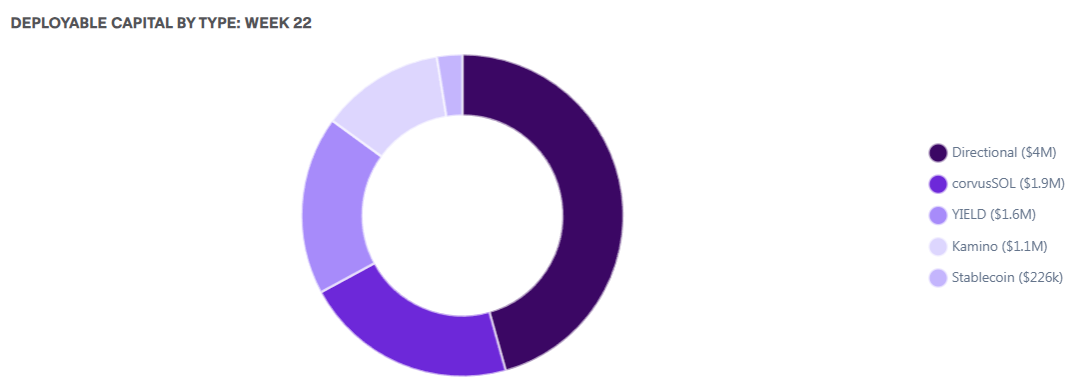

This chart shows how the roughly $9M of deployable capital is distributed across strategy categories, with directional strategies accounting for the largest share (~$4M), followed by corvusSOL, YIELD, and Kamino campaigns.

This chart compares the number of active strategies by category across Weeks 21 and 22, showing growth in directional and Kamino strategies, declines in YIELD and corvusSOL strategies, and a net increase of two total strategies.

Winners and Losers

Biggest Winners

JLP Long: 11% → 95%

BTC Long: New at 25%

USD / USDT*: 9% → 10%

STKESOL ecosystem strategies continued improving

Biggest Losers

JLP Short: 34% → −2%

ETH Short: 32% → 10%

corvusSOL / SOL: 49% → 37%

YIELD / SOL: 42% → 35%

The largest moves were driven by the surge in JLP yield and the normalization of campaign rates.

What We’re Watching Next

Three metrics will likely determine Week 23:

Can JLP maintain a yield above 12%?

Will STKESOL continue gaining ground on YIELD?

Can SOL borrow rates remain below 7%?

These factors now drive the majority of strategy performance across the platform.

Final Take

Week 22 marked a major rotation in the platform’s opportunity set.

JLP emerged as the dominant source of yield, stablecoin strategies became more attractive as borrowing costs fell, and STKESOL strengthened its position as the most resilient campaign asset.

The platform is becoming less dependent on incentive-driven farming and increasingly focused on revenue-backed yield, efficient stablecoin deployment, and directional market exposure. Those themes are likely to remain the key drivers heading into Week 23.

Start to use a unified margin infrastructure, your capital works better that way. Try it today !